As 2026 approached, global investment markets expected late‑2025 trends to continue. Inflation was projected to decline, policy rates to ease gradually, and growth to remain steady but uneven, with market leadership broadening beyond the prior year’s narrow focus.

However, the onset of the Iran war dramatically changed this outlook, intensifying significant geopolitical risks and compelling investors to reassess uncertainties around energy supply, disruptions in shipping and security, and the possibility of rising inflation.

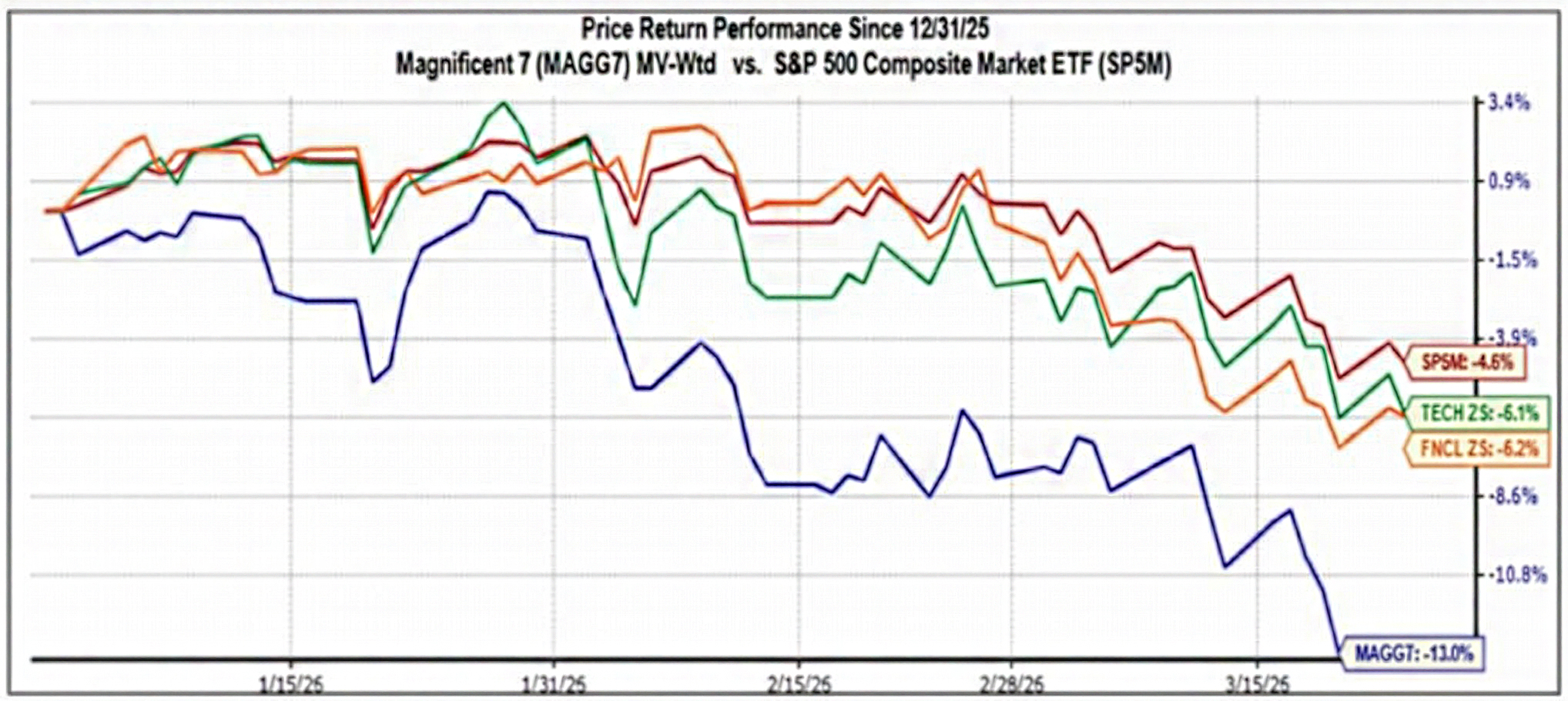

Equity Markets

Chart provided by Zacks Investment Management, April 4, 2026.

In the first quarter of 2026, developed market equities experienced a decline of 3.5%. This drop was primarily led by the S&P 500, which fell 4.3% amid significant investor rotation away from mega cap technology stocks—a trend reflected on the corresponding slide. The movement was driven by mounting concerns about the scale of capital expenditures related to artificial intelligence and doubts about the long-term sustainability of software business models. U.S. large cap growth stocks saw a notable decrease, falling 9.8%, which was nearly 12% worse than their U.S. value stock counterparts. The "Magnificent 7," highlighted in the slide, fell by more than 11% during the quarter.

European equities declined by 1.2% for the quarter. Gains early in the year, driven by better growth sentiment and reasonable valuations, were offset by a sharp drop late in the quarter as the Iran war pushed energy prices and interest rates higher. Europe’s lower valuations and its value/cyclical sector focus helped soften the impact, with resilience seen in energy, defense, and financials, while rate-sensitive and global sectors faced greater challenges.

Emerging market equities showed resilience, falling just 0.1% amid broader market volatility. Asian equities outperformed thanks to technology sector growth, while Latin America was affected by commodity price swings and geopolitical disruptions. Despite regional divergences, stable monetary policy and sectoral strength helped emerging markets remain steady during a turbulent quarter.

Commodities markets emerged as the leading asset class, with the Bloomberg Commodity Index advancing 24.4% for the quarter, primarily fueled by a significant rise in oil prices. Gold dipped almost 20% from late-January highs but still posted a 7% quarterly gain.

Interest Rates

As the Iran crisis began, 10-year U.S. Treasury yields jumped 0.50% to 4.49% as markets adjusted for an oil-induced inflation shock and rapidly revised their expectations for Federal Reserve rate cuts. Rather than seeking U.S. Treasury safe-haven assets, investors required greater compensation for both inflation and duration risk, resulting in a widespread selloff of government bonds across the yield curve. U.K. and euro-area bonds experienced steeper selloffs than U.S. Treasuries due to their greater sensitivity to energy-price shocks, resulting in larger and faster increases in yields.

U.S. credit spreads widened across both investment-grade and high yield as recession and inflation risks rose, though these moves were very moderate compared to the sharp jump in Treasury yields. The selloff remained orderly given strong fundamentals and low near-term refinancing needs. Pressure is most acute in energy-importing sectors and lower-quality credits, but no systemic stress has emerged.

Private credit has faced increasing challenges, particularly as investments in the AI and software sectors prompt questions regarding capital expenditures and underlying business models. In response to volatility, several funds have tightened redemption restrictions to protect liquidity, emphasizing the need for careful sector and risk management as confidence in tech-related credit declines. Ultimately, the effect depends not only on sector exposure but also on manager expertise, making manager selection vital for managing risks and preserving stability in private credit strategies.

Central Banks

Central banks have quickly adopted more cautious approaches, though their strategies have diverged. The Federal Reserve has held rates steady, adopting a “look through” approach to remain flexible, carefully considering elements such as inflation, shifts in employment trends, and the United States’ status as an energy-independent nation. The Federal Reserve held rates steady at its most recent meeting, and recent commentary suggests policymakers are unlikely to move unless there is clear evidence that inflation is falling, or that the labor market is weakening more materially. The bottom line, in our view, is that earlier expectations that the Fed would lower rates at an upcoming meeting are fading fast.

Other major global central banks have shifted into a more cautious stance focusing on the potential inflationary effects of the conflict. The European Central Bank has moved to a vigilant, inflation‑first posture with rate cuts off the table, while the Bank of England has paused its easing cycle and is monitoring energy‑driven inflation risks without rushing to tighten. In contrast, the Bank of Japan remains broadly accommodative, prioritizing economic stability while closely watching energy prices and currency pressures rather than signaling near‑term policy tightening. Overall, global policymakers are emphasizing flexibility and inflation control amid heightened geopolitical uncertainty.

Diversification

Over the last five-to-seven years, equity market returns have been heavily influenced by a narrow set of better-performing themes, most notably U.S. mega-cap technology and growth. While that concentration has benefited performance, it can also create hidden risk. When market leadership rotates, a portfolio that is heavily tilted to yesterday’s winners may experience larger drawdowns and fewer sources of return to stabilize results.

Prosperity portfolios are intentionally diversified across asset classes, regions, and equity and fixed income so that outcomes are not dependent on any single theme continuing to work. Despite high levels of volatility, client portfolios are flat-to-down slightly. Further diversifying our equity holdings by adding more exposure to international equities in the summer of 2025 and maintaining high-quality, duration-neutral fixed income allocation has provided better performance.

Diversification does not eliminate volatility, but it helps control risk by spreading exposures across different drivers of return: growth, inflation, interest rates, and credit conditions; so that no single shock dominates the portfolio. In periods like the current environment, when inflation, rates, and geopolitical risks can change market trends quickly, a diversified allocation is designed to be more resilient and to keep investors positioned to participate as opportunities broaden beyond the narrow set of market leaders. The discipline is to stay invested, avoid chasing what has already outperformed, and rebalance as markets move, maintaining exposure to multiple return sources so the portfolio can adapt as conditions evolve.

Cease-Fire

On April 8, a cease-fire was declared, marking a hopeful step toward ending ongoing hostilities. However, its longevity remains uncertain. The length of the conflict will likely be a key factor influencing market performance, as it will determine if the current energy shock is only temporary or becomes a persistent challenge for the broader economy. If tensions persist and disruptions continue in the Strait of Hormuz, elevated risks and volatility are expected to remain, leading to greater swings in energy prices.

A Focus on Resilience, Not Predictions

For client portfolios, we’re focusing on staying diversified and flexible rather than making big directional bets. We’re balancing growth opportunities with assets that can hold up if interest rates stay higher for longer, and we’re avoiding over‑reliance on any single outcome for the economy or the Fed. We’re also being thoughtful about interest‑rate exposure, favoring approaches that can adapt if rates move in fits and starts. Overall, our goal is to help portfolios participate in market opportunities while remaining resilient during periods of volatility, rather than trying to time short‑term market moves.

Securities offered through DAI Securities, LLC, Member FINRA/SIPC. Advisory Services offered through Prosperity – An EisnerAmper Company. Prosperity – An EisnerAmper Company is not affiliated with DAI Securities, LLC.